Central London overview

Across London, the negative trends seen in the first quarter have not only continued but are beginning to really gather momentum in most locations as companies analyse their internal costs, unemployment is on the rise, interest rates are increasing, inflation at crazy levels, and the wider society is less than happy. This is a bleak picture where commercially the negative impact will gather momentum at pace.

For office space this can clearly be seen in the periphery markets around the core markets in the City and West End, where rents are moving down, incentives are moving out, and lease lengths are becoming shorter and shorter. Essentially anything that isn’t the very best space of all sizes, and /or anything under circa. 5,000 sq. ft. that isn’t a true Cat A + product is having a torrid time. On the bright side however, occupiers are beginning to see far more amenable terms than perhaps they have become accustomed to.

Market Rents

The continued adoption of remote and flexible work arrangements has prompted occupiers to reconsider their office space requirements, leading to a diversification in leasing preferences.

Market rents reflect this changing landscape, as Grade B stock within fringe locations experience moderate downward pressure due to reduced demand. However, demand for innovative and amenity-rich spaces in prime submarkets remains resilient, influencing slightly increasing rents. Landlords are adapting by enhancing property offerings to cater to occupiers’ evolving needs, such as integrating advanced technology, wellness features, and eco-friendly designs.

Additionally, the sustainability agenda has gained prominence, with tenants valuing environmentally responsible buildings and landlords incorporating green initiatives. The market also indicates a trend towards shorter lease terms, enabling occupiers to maintain agility in uncertain times.

Some evidence of said resilience can be shown by the fact that record rents have recently been achieved, including the Partners Group acquiring c. 38k sq. ft. at JJ Mack Building at a rent of c. £100 per sq. ft. We also saw Chanel double the size of their London HQ to 86k sq. ft. after agreeing a 20-year lease at 38 Berkeley Sq. at an undisclosed rent close to £185 per sq. ft.

Leasing activity

Much like Q1 2023, whilst initial activity has been well above the COVID levels, overall activity remains subdued. Q2 has seen more than 2.2 million sq. ft. transacted. Despite this sizeable number, this is circa 30% drop in the same quarter the year before. When looking on a longer-term basis, this is 25% below the 10-year 2nd quarter average which is well above 2.65 million sq. ft. Taking stock in the year to date, take up as been more than 4.1 million sq. ft., which is 26% lower than the first half of 2022 and is 20% below the 10-year average of 4.9 million sq. ft.

Much like the previous quarters we have continued to witness a strong pre-let policy especially for the larger occupiers who are seeking a superior product whilst reducing their overall footprint as the workplace continues to react to agile working. To quantify this, we have seen 14 pre-lets taken place in Q2 2023, which equated to circa 490,000 sq. ft. and represented a quarter of overall Q2 leasing activity.

Most notably, 1 Leadenhall in EC3 on behalf of Latham and Watkins, 1 Liverpool Street, EC2 on behalf of Dentons, and 38 Berkeley Square, W1 on behalf of Chanel.

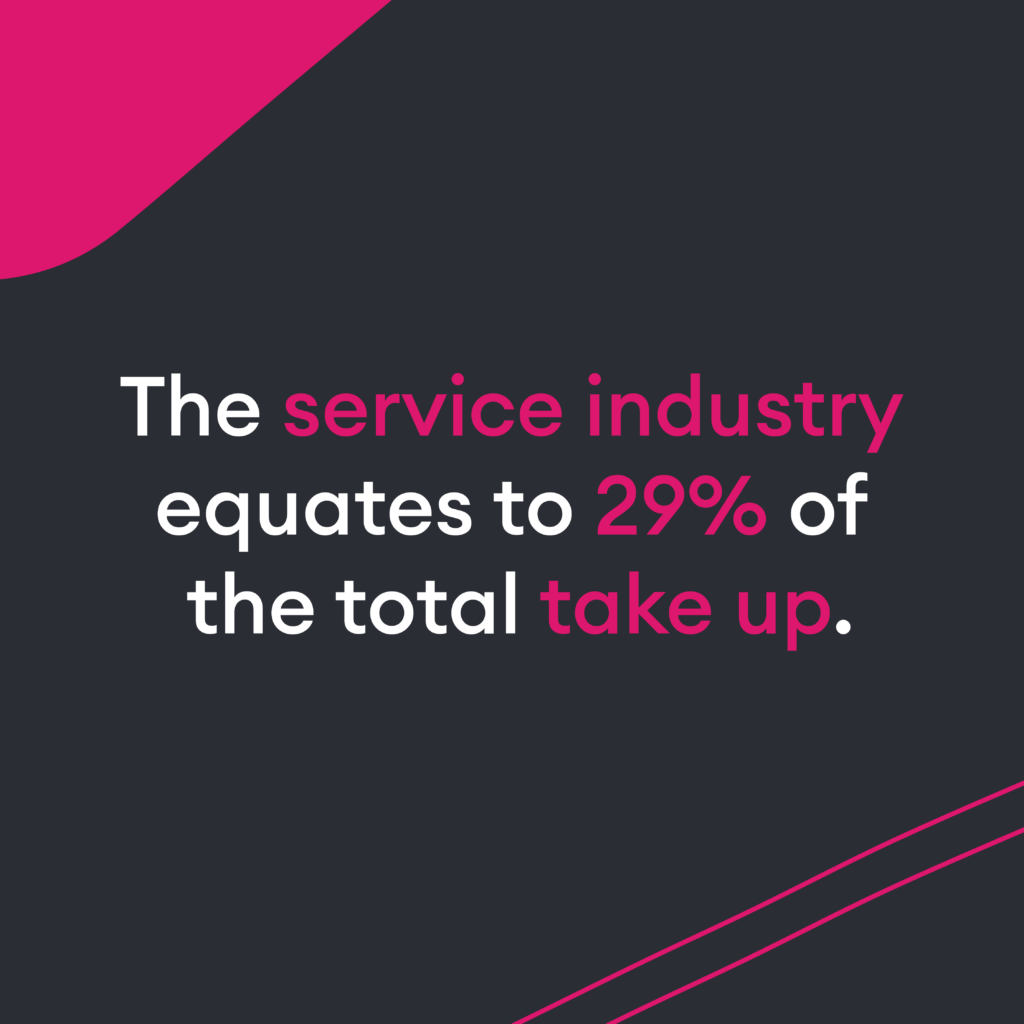

If we were to breakdown take up by industry its clear the service industry has been the most active. Gone are the days of Law / TMT and Banking leading the way and this is largely down the ever-worsening economic climate and a switch to agile working. It is reported the service industry which includes the likes of leisure, insurance, and property (serviced office market) equates to 29% of the total take up. The professional sector was a close 2nd at 22% and the banking and finance was 3rd contributing circa 19% of the overall take up.

As we look forward it’s difficult to predict the state of the property market as the UK and the world continues to deal with the fallout of COVID and ever rising inflation. With that in mind, it’s extremely hard to accept anything other than continued subdued activity. What’s interesting and perhaps a glimmer of hope for some optimism, the long-term average for currently under offer stock is at its highest levels, well above the long-term average. Which suggests a strong 2nd half of the year.

With the above in mind, we fully expect the following topics to continue grow in momentum.

Shorter lease lengths – we have seen the average term certain across central London shrink significantly. In 2019, it stood at 5.5 years, whereas at the end of 2022 this had fallen to 4.2 years. Much like the immediate year or two post COVID, sublease space will continue to increase as the economic downturn causes further pressure on occupiers.

There will be a continued reliance on fitted office. This began during the uncertainty of COVID as landlords looked to compete with the sensation of serviced offices. Not to mention the significant savings for occupiers in terms of CAPEX from inception of the lease and the savings on dilapidations at the end of the term.

Vacancy rates and availability

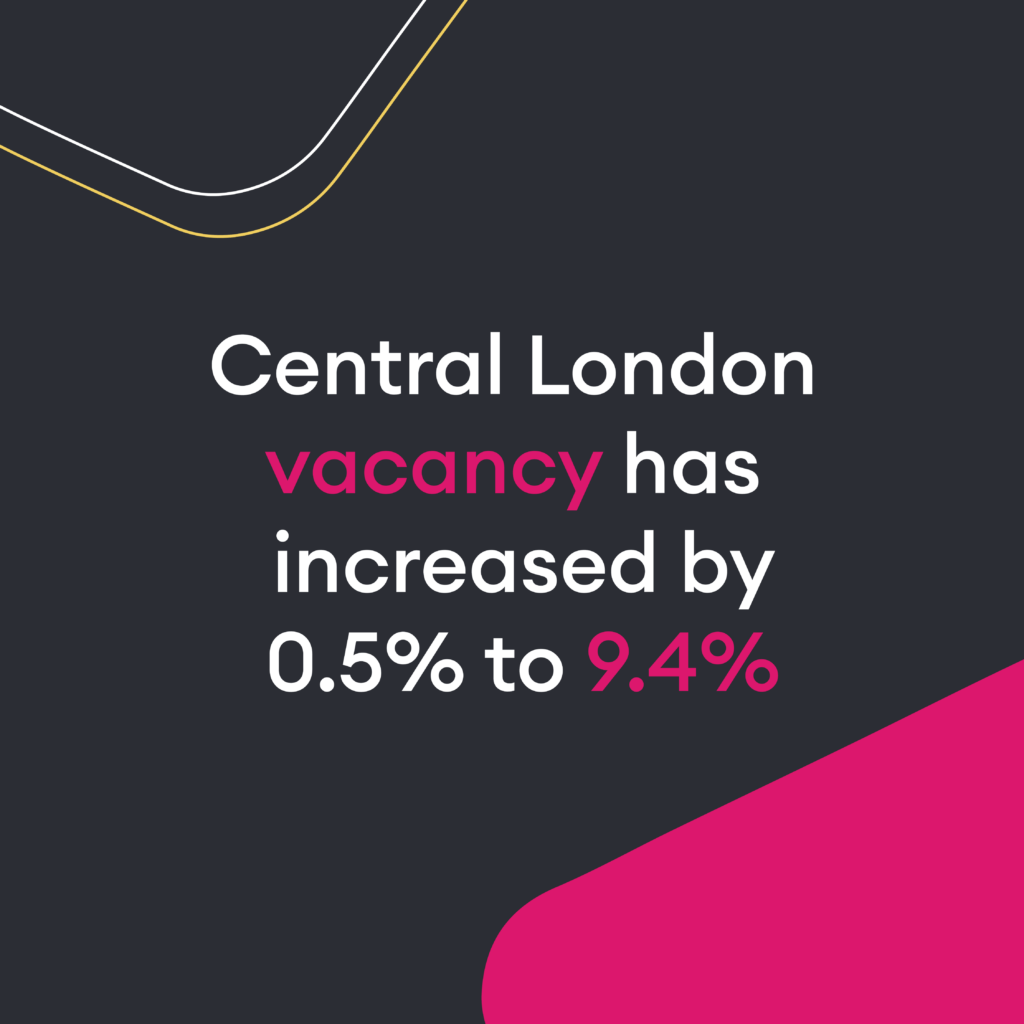

Another quarter, another increase in availability! Central London vacancy has increased by 0.5% to 9.4%. However, the flight to quality is still consistent. This is a result of the completion of some newly built stock and the increase in the availability of refurbished stock. Availability in the capital is approximately 50% higher than that of pre-pandemic levels and higher than the national average at 8.9%. The forecast on vacancy rates and availability of all use classes over the next 12 months looks bleak with more space coming to market with a final levelling off in 2025. We could see vacancy rates tipping over 11.5% if things continue as they have been.

Sales Market

The Investment and sales market is continuing to struggle within the capital and is illustrated by a further reduction in activity during Q2 2023, falling by approximately a third in comparison to one year prior. To quantify this, the total value of sales across London was £3.5 billion – highlighting a total volume 41% lower than the 10-year average. This is compounded by yields continuing to soften throughout all submarkets in London with Central London offices. Central London yields are hovering around 5.3% on average.

Experience allows us to understand that this is driven by several factors ranging from changing is workplace strategy to rising inflation and interest rates. It will be interesting to see how the market reacts to the number of properties that might be under pressure if and when they get into trouble and if they need refinancing. Nevertheless, there is still activity and two of the most notable deals were 60 Gracechurch Street which was purchased by Obayashi Corporation for £140m (4.7% NIY) and the sale of 50 Finsbury Square for £190m (4.4% NIY).

Development pipeline

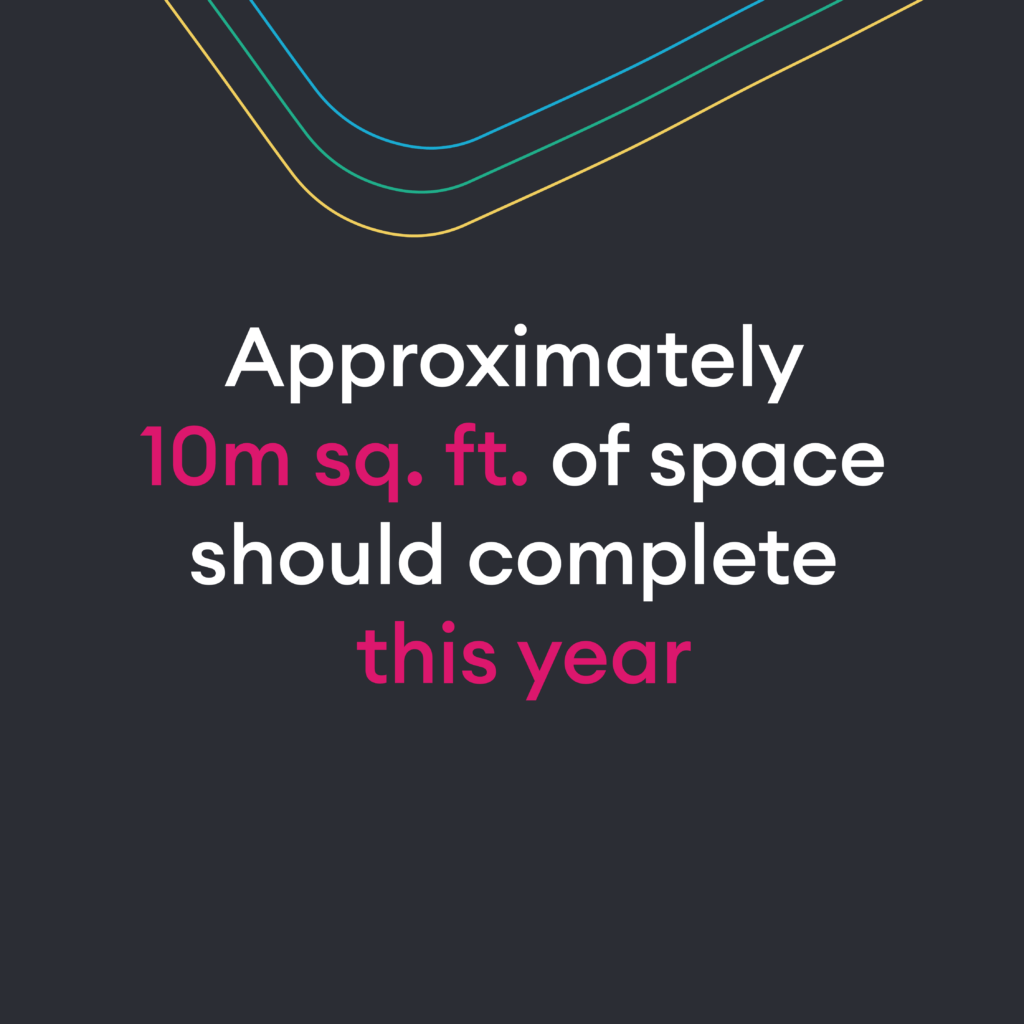

2023 is continuing its relentless pursuit to become the busiest year for new development completions in the last 20 years. Approximately 10m sq. ft. of space should complete this year which is around the same amount of space that completed when Canary Wharf/Docklands was completed back in the early 2000’s. That may sound a lot of office space, in the wake of the hybrid/WFH model that is sweeping the country, however around 50% of these completions will already be pre-let prior to fully completing. This shows that there is still an appetite for offices providing they are creating what occupiers want.

These new builds are aiming to bring in a new wave of office buildings with high ESG credentials, in readiness for the new regulations on EPC’s coming in the next 4 to 7 years.

However, most of these buildings were ideas conceived pre-pandemic (think of Google’s new Kings X campus) and we are now entering a new world where interest rates are much higher, the cost of everything is higher due to inflation and demand is not what it once was. As such we should expect to see the number of new developments wane and approved planning permissions delayed until developers can seek beyond the spiralling cost of developing these new buildings, especially when their potential rental returns cannot be realised as well as they used to.

No doubt most people think of the City as being the focal point of new developments, mainly due to the media spinning out the usual ‘tallest tower’ chat, however the City only makes up 25% of the 10m sq. ft. completing this year, the West End has 20% of the new developments per sq. ft. with Midtown (10%), Southbank (5%) and Docklands (5%) taking their fair share. The scheme that SHB will be looking at closely is the development of Cole church House in London Bridge as that will complete the area directly outside the station. Other notable schemes outside of the main core areas that are just kicking off are Gateway Central in White City and the long awaited and long planned Kensington Olympia scheme.

Industry analysis

Analysing SHB data on new client enquiries & new instructions throughout Q2, it’s been a great mix of various sectors all analysing their real estate strategies, however very few are looking to take up more space than they currently have as the trend of Rightsizing continues. Our top sectors were Finance (inc. Fin-Tech), Technology & Recruitment.

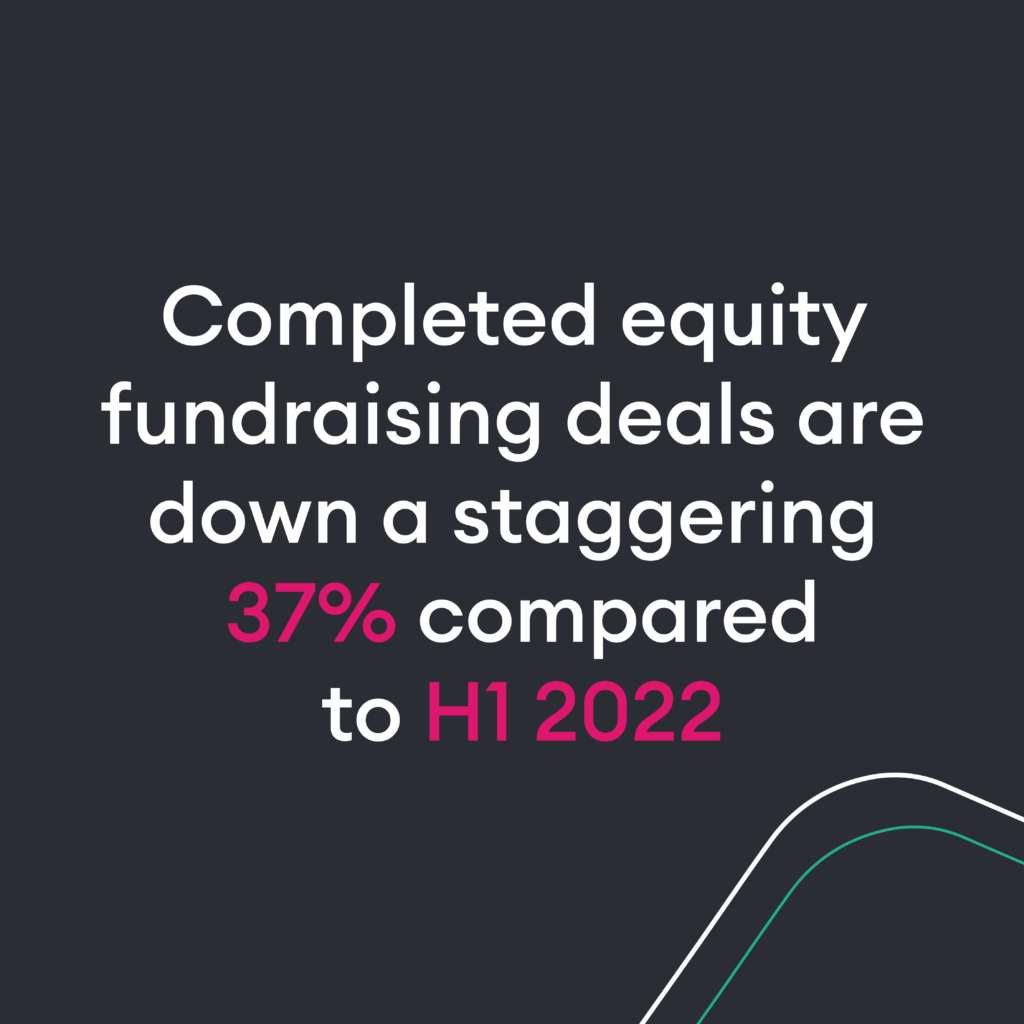

In the first half of this year, completed equity fundraising deals are down a staggering 37% compared to H1 2022 with only 1,094 deals completed and the actual amount raised down almost 78%. This is particularly worrying for those seed stage start-ups and even more worrying for firms that would be expecting their second or third rounds. Almost certainly this will lead to layoffs across the big sectors relying on funding, Fin-tech being the sector that has seen the biggest fall, followed by Life Sciences & Cleantech. Despite public scepticism & scrutiny, Blockchain is the only sector that saw a rise in the number of deals completed compared to the same period last year perhaps indicating where things are going.

The buzzword sector of this year ‘Artificial-Intelligence’ is still performing relatively well in the investment leagues despite a drop-off, the amount of deals complete still exceeds 2021 levels.

The impact we are seeing on the ground when it comes to analysing the impact of the above on occupier movement within the office market is certainly that the smaller firms moving and scaling in serviced office space has slowed down significantly. Either extending in their existing space, moving back to a WFH model or continuing using hybrid rotation as a longer-term solution.

Whilst interest rates continue to rise there appears to at least be some certainty and an understanding on how things are going to play out & how long this downturn will last, allowing occupiers cross-sector to start planning again. That paired with the amount of available office stock on the market in the 2,000-10,000 sq. ft. bracket offering a Managed Solution or additional flexibility on a conventional basis, is allowing movement & transactions to happen as decision making becomes easier on both sides.

Flexible workspace

Q2 has been a challenging period for the flex market, as it seems that enquiries have been decreasing across the board. However, it’s worth noting that deal volume hasn’t been significantly impacted yet. Nevertheless, we might anticipate a quieter Q3 as people continue to figure out their staffing needs.

Currently, the major issue companies are grappling with is the existence of unused office space during certain days of the week, and there’s no sign of flexible working policies slowing down. Most businesses report that the office is only being utilised for 2 to 3 days a week. This situation is paving the way for flexible booking platforms to step in and cater to overflow needs when maximum capacities are reached. Another approach being adopted is staff rotation, which, unfortunately, might reduce the cultural aspect of the office.

Finding a one-size-fits-all solution is proving to be elusive now, and we anticipate that the greatest challenge for occupiers in the upcoming months will be determining the most suitable approach to accommodate both growing and shrinking teams. This decision will have significant implications on how businesses operate in this evolving landscape.

A roundup from SHB’s CEO

ROLL UP ROLL UP, BAD NEWS EVERYWHERE YOU LOOK OR HEAR. It really is enough to make one climb under a rock until it all goes away! There is however another way of looking at this in that this is a period of correction that is entirely necessary in a capitalist society. Although daunting, there will be the kind of enlightening opportunities, the kind we haven’t seen for a very long time. This is triggering in the most exciting of ways for people that are not daunted by the disruption that such a correction is likely to bring. Unfortunately to get to good things, we must go through some tough times.

As a wider community we need to be realistic about what we are dealing with. For example, celebrating and breathing a united sense of relief every time we miss the definition of a recession by the smallest of blip, is not particularly useful. Some things are far worse than recessions, and what we are experiencing is a long downturn, with a deep myriad of layers. This isn’t really an issue in the sense that the tough times are as necessary as the good times, but this is a downturn that really packs a punch for several reasons. Not least of all due to the necessary corrections because of our numerous financial interferences all the way back to the banking crisis. As such what we might be witnessing is a true recalibration, which currently has little sign of becoming any easier.

In fact, it is more likely that much of the real pain has not landed yet, and surely in the coming months (perhaps years), we will see unemployment quickly rising, house prices falling, and of course commercial rental levels and capital values dropping. Scary stuff or highly opportunistic or both? This is for the individual with their own circumstances to decide, but in the short to medium term, if you see fit (and in most cases advisable) – get back into the office and buckle up. Hard work and perseverance will bring results!