Central London overview

The run into the break was good for many, as deals were pushed over the line, and celebrations were had over steak and egg nogg. However, going into the Christmas break in times of uncertainty there is often a sense of concern about what the tone of the markets will be when we all return in early January. The break itself can often be a transitional moment, and over the first few days in January, it felt clear to most that all was not well. Indeed, the shiny instructions in most core markets have still been going great guns, but as we stepped through the quarter, the undercurrent of market feeling on the sub-prime stock was starting to feel as dreary as the weather. As the drizzle continued to come down, the all too familiar slow-down of decision making, seemingly driven by companies analysing their costs, really kicked in.

This is not at all to say that transactions haven’t been happening. They certainly have, but in January they were largely legacy transactions for decisions that had already made. By the time we got to the end of the quarter these deals had been done and we saw decision making really starting to slow, lawyers went into another level of taking time to do deals, availability increased, voids moved out, and rents in some areas started a downward trend.

What has become even clearer, is the ever-increasing movement of occupiers wanting Cat A+ space. It really is becoming an office revolution, with those Landlords that are prepared to spend the necessary money, getting their returns in both minimising voids and increasing their rental profiles. Not only that, but it appears to be spreading to larger spaces. The older concepts behind speculating to accumulate is finding its feet again, and occupiers are understandably enjoying the attention, and they are ultimately prepared to pay more for the privilege. For now, this trend works for everyone, but some landlords just won’t join in the fun, and it is likely that they will lose out as a result.

Market Rents

Prime and top rents continue to see upward pressure due to competition for future-proofed products. With new MEES regulations taking effect in April, the focus on sustainable, compliant, and energy-efficient stock will only intensify, putting further pressure on a pipeline that while growing, is still subject to external funding and profitability challenges.

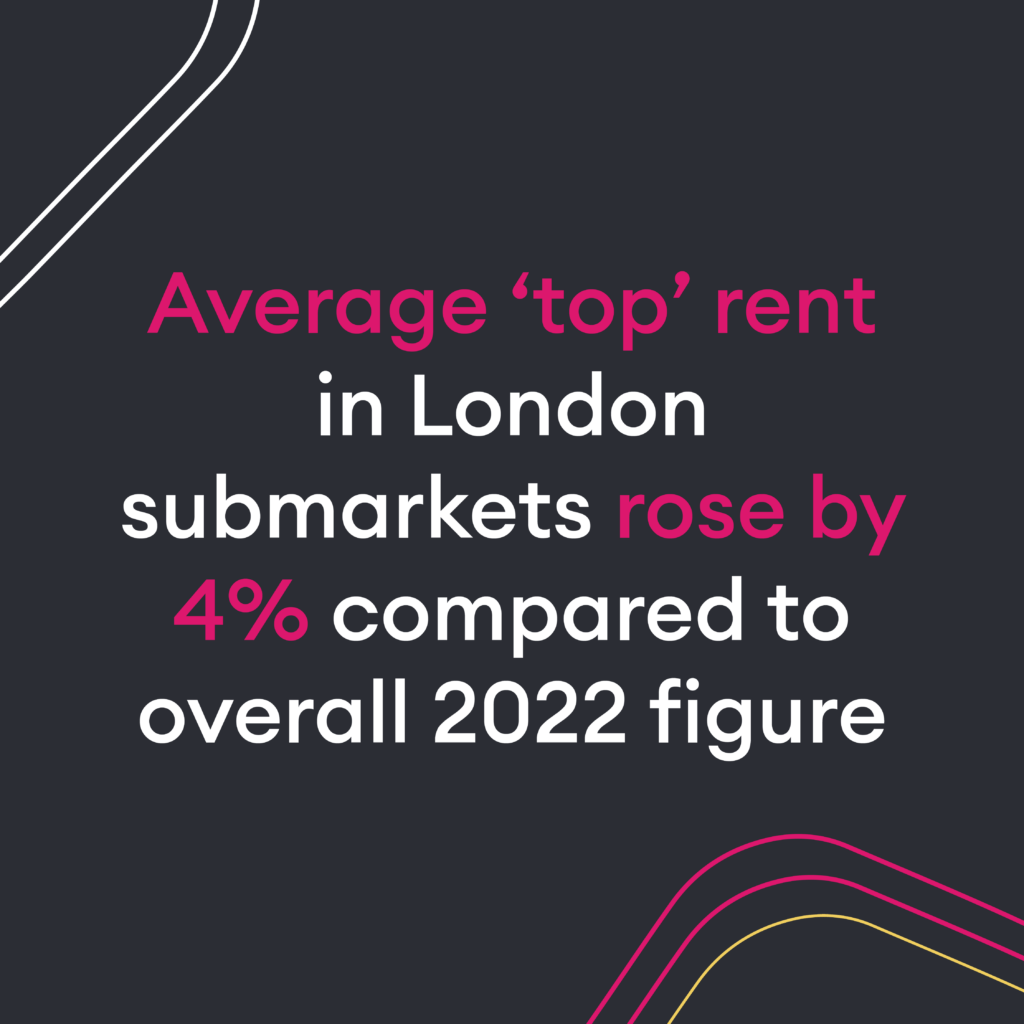

The average ‘top’ rent achieved in all core London submarkets was over £102 p/sq. ft. which denotes a rise of 4% compared to the overall figure for 2022.

Focusing in on the West End market, premium rents continue to be achieved at keynote schemes in the core West End such as upper floors at 65 Davies Street (£165 p/sq. ft.) and 5 Hanover Square (£150 p/sq. ft.). Overall prime rents for mid-level floors remained stable in Q1 but despite the volatile nature of demand, we still see potential for rental growth given the continuing occupier search for best-in-class products.

Over in the city, prime rents ended 2022 at £72.50 p/sq. ft. but Q1 has seen the first upward movement for three years, as they reached £75 p/sq. ft. Occupier appetite for new Grade A, while not at levels being experienced in the West End, is still creating competition for quality new stock. Premium rents continue to be achieved on upper floors at high-profile schemes.

Leasing activity

The London Office Market continues to recover from a significant hangover caused by the dreaded COVID, which burdened the market with a massive shortfall in demand. Thankfully, as the general stigma/fear associated to the virus and government restrictions have eased, employers and employees are becoming increasingly comfortable with returning to the workplace. This has helped bring a drop in availability as occupiers have continued to withdraw their offices from the subletting / assignment market.

Thankfully, there have been several occupiers who are driving this resurgence in demand including the likes of the Technology, media and law firms driving demand especially on the larger end.

Despite the above, conditions remain tough. To put this into perspective, availability is circa 50% above the pre pandemic level. With vacancy running at about 8.8%, which is at a 15-year high, compared to the previous average of 5%. Whilst for the first time in a long time, net absorption has been positive, which has helped the vacancy rates, vacancies continue to rise as new stock is delivered to the market.

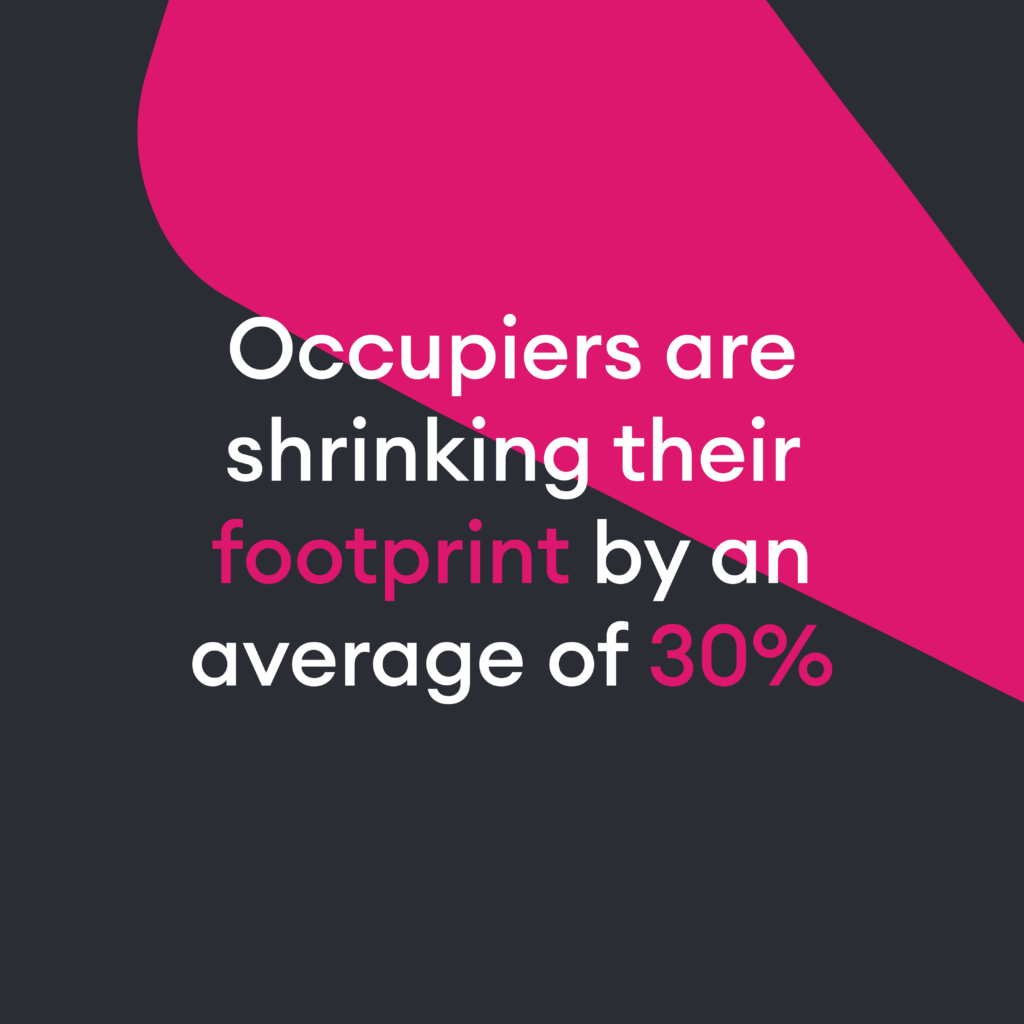

Much like the majority of last year there remains a 2-tier market. With many occupiers opting for a superior product to that of their previous office, with a specific emphasis on the sustainability / ESG perspective. Interesting enough, SHB saw occupiers shrinking their footprint by an average of 30% as they react to the new norm of agile working. According to the statistics net absorption for 5 Star buildings since the emergence of the Pandemic has remained positive, which is a stark opposite to the older, 2nd hand market, so much so there is more than 10,000,000 sq. ft. of lower rate offices available on the market.

As mentioned previously, it’s been the likes of the Technology and Law firms which have been the most bullish in their office movements. With many taking advantage of the uncertainty surrounding the market. An example of which is Clifford Chance who later went on complete one of the largest office acquisitions in recent years, back in November 2022, having pre-let 328,000 sq. ft. at No. 2 Aldermanbury Square. They vacated 700,000 sq. ft. in the Docklands. A classic example of an occupier far improving their office whilst reducing their overall footprint considerably. Elsewhere, Reed Smith took 130,000 sq. ft. in the city, having downsized from 170,000 sq. ft.

This can be compared to the Bank and Financial Companies, who are also reducing their overall footprint. Back in Q3 2022, Blackstone Pre-let 225,000 sq. ft. from BIA at Berkeley Square. Barclays will be exiting from 500,000 sq. ft. in Canary Wharf, and UBS requiring sublease space at No. 5 Broadgate and JP coming out of their office in Knightsbridge, Aviva have also confirmed that they will be consolidating into a smaller space.

As we look forward, it’s difficult to see anything changing at least significantly over the coming year. The country remains burdened with inflation and uncertainty both of which can have an adverse effect on businesses and in turn the office market. Historically, albeit there tends to be a slight delay before any trends and sufficiently realised in the office market, economic downturns will result in a continued decrease in activity, driving availability up and rents down!

Vacancy rates and availability

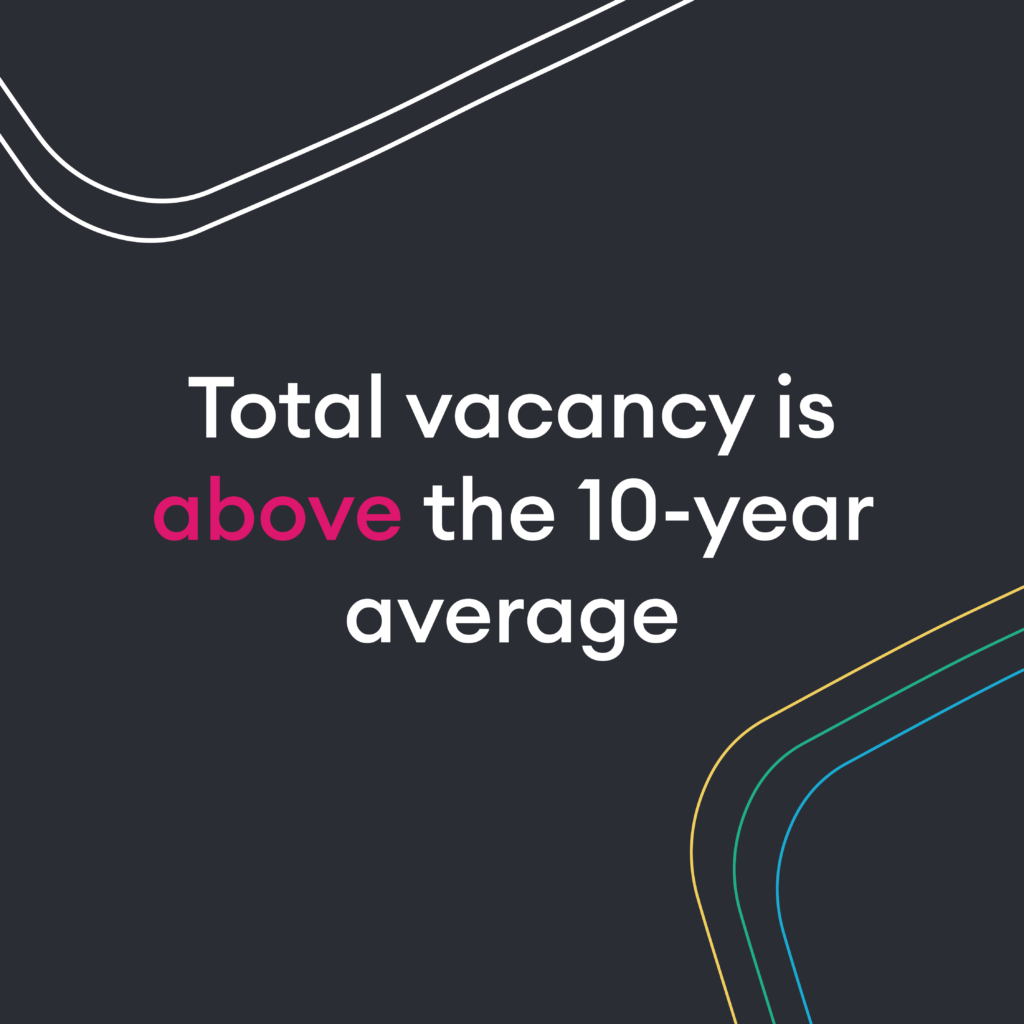

The overall supply continued to increase by between 5-6% during Q1 to approximately 23 million sq. ft. There continues to be a two-tier market where in many locations, there is a lack of good quality stock and therefore take-up is being impacted. The key component impacting the increase in supply is driven by the upward trajectory of second-hand stock and many of the offerings are larger buildings and floorplates. Ultimately, the total vacancy is above the 10-year average which is clearly driven by the volatility in the economy and an increase in occupational costs. New built stock vacancy remains low but is still slightly higher than the 10-year average of an estimated 1%.

Sales Market

After a very quiet end of 2022, the first quarter of 2023 has not exactly kicked into life but merely limped into the New Year. Rising interest rates have dampened investors’ expectations as values have been cut across the board and it has created an environment where financing new projects becomes harder and harder to justify. Proven locations like Tottenham Court Road/Soho and the City Core are still attracting investors though with a couple of notable acquisitions being GPE’s acquisition of 1412 Wardour Street and Allianz House in Gracechurch Street being sold to a Japanese consortium.

A lot of deals being lined up slowly in the last quarter have yet to come to fruition and pretty much every single one of them has seen pricing and debt having to be restructured to try and get deals over the line. Investment agents, who had their feet up most of the end of last year, are now having to work even harder to get deals over the line as many investors are being spooked by the smallest of things and using them as an excuse to pull things. It would appear the area not to invest in now is Docklands and Canary Wharf where the vacancy rates are rocketing and demand is just not there, fuelling an area which could see some significant rental value decreases in the coming months.

Development pipeline

Currently there are circa 4.3-4.4m sq. ft. of new constructions committed in Central London over nearly 50 different schemes. This does also include refurbishments and one of the largest to be undertaken is the Citigroup refurbishment of 25 Canada Square which takes up 900,000 sq. ft. of the above figure.

Due to supply chain issues and the cost of materials, we have seen several projects get delayed into 2023 that were previously supposed to complete in 2022 so this year we could see records amount of schemes either complete or start compared with previous years. Now we’re estimating over 10m sq. ft. of space to completed at some point this year.

There is increasing pressure being put upon developers, landlords and owners to ensure that their buildings are adhering to the new EPC and ESG regulations being put in place over the next 5-7 years and those owners are starting to put things into place. From April 2023 you cannot now dispose of a building which has an EPC rating of E or below unless it’s listed or exempt for any reason. This requirement will increase to B eventually which puts tens of thousands of buildings in the firing line for an upgrade.

With the levels of take up usually seen in the market, what we could be seeing is a large amount of space hitting the market at the same time as more tenant space being dumped onto the market and a resulting dilution of the market generally.

This year could be really interesting and a real benchmark as to how the market will shape up for the next few years as we have a cauldron of increased supply, weakening demand, occupiers fighting with their employees to get them back into the office, the buzz of inflation weakening but finance being less easy to come by and an economy on the brink of something but no one knows quite what yet. Throw in the diplomatic turmoil of wars, as well as looming elections in the US and UK and we have quite the cauldron.

Industry analysis

Activity continues to remain strong in London’s top performing sectors for Office Take-up with Finance, Legal & Tech firms leading the way yet again. In past years the activity from these sectors would be making huge dents into vacancy rates of space in London, but as mentioned within the Leading Activity section, a lot of the moves & transactions taking place are part of firms ‘Right-Sizing’ – efficiently reducing their occupational footprint in exchange for better quality buildings or a more prestigious location. Big names within the tech-sector surprisingly & publicly announced their intentions to get staff back to the office which has helped with activity & looking at own data, a lot more to come as we head into the new financial year.

Sub-sectors such as Artificial Intelligence & Life Sciences continue to receive VC/PE interest & large sums of investment leading to increased headcount & inevitable requirements to review their office footprint – their activity within the London office market has been significant, especially with our own teams consulting for 3 out of the top 10 AI firms in Q1 alone. Life Sciences continue their pursuit of more & better spaces in the regions with Cambridge being the most active market historically and for some time to come.

There will be a real mix of activity within the leasing market over the next year cross-sector as all the firms who signed their lease just before Covid in 2019 start to approach their 5-year lease break/lease end and will no-doubt be advised to use these events to their advantage which so many have already made a start on. Sectors performing particularly well & predicted to grow in the coming year will include the top 3, joined by Consumer Staples, Energy & Healthcare.

Flexible workspace

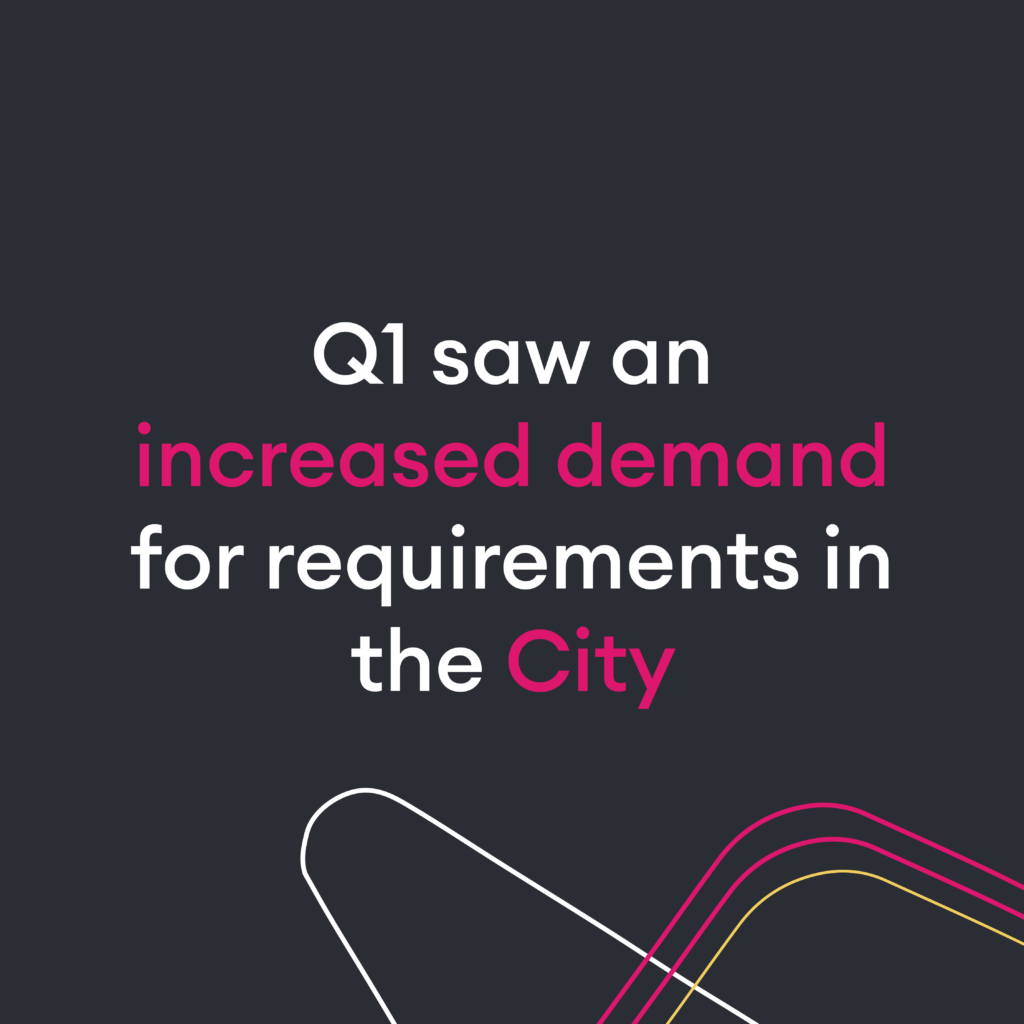

Q1 saw a real uptick in demand for the city, as the slowest market to rebound post-covid finally started to garner interest from current residents and others who had maybe been priced out of the hyper-competitive West End markets.

Whilst demand intensified across the board, decisions were still taking longer than expected. In several cases, companies waited while they tried to get a better steer on where the market would be. This was to be expected after a turbulent 2022 and is something we’re now seeing clients try to combat by starting their office conversations earlier.

In the Flex market, you would typically need 3-4 months from initial enquiry to occupation but as we see more people make the move from traditional lease space to the Flex market, these occupiers are enquiring earlier to fall in line with their notice periods. Providers of larger, Managed, offerings are now trying to bridge that gap by showing their upcoming stock much earlier than they previously would have.

A roundup from SHB’s CEO

At SHB we have some very clear internal metrics about transactionally what is coming through the market. We have developed for our own use, various platforms to monitor occupier movement. To support this, we also have an extensive team of researchers, as well as Client Solutions callers, whose role is to develop and uncover opportunities for SHB to represent parties with imminent lease events. By the end of the first quarter of 23, it was clear that our bookings of new opportunities had decreased by around 25%, based on our mean average. Not only this, but the length of time that deals were taking, extended out significantly from around 6 weeks to a worrying 8-10 weeks. Everything has been laboured and decision making has not been forthcoming, and the reasons are varied. (Not just down to lawyers). On reflection, it appears largely driven by occupiers looking closely at their internal cost base, then following their findings, deciding on a strategy to reduce costs. This likely reduction in head count, mixed with the modern-day confusion on how to use commercial space (coworking, collaboration, working from home vs not working from home etc etc), as well as falling financial returns, has led to occupiers not wanting to commit with confidence to pretty much anything. Furthermore, increased cost through the worst sustained inflation in many generations, the war in Ukraine, the rising storm of strikes, as well as companies carrying significant historical debt. All in all, the landscape is depressing, and there seems little reprieve.

Recession or Not Recession, that is the Question?

As a society, we have benchmarks that acknowledge good things and bad. If we avoid a recession, which we have in recent times, then we tend to breathe a sigh of relief and the market narratives across all sectors seem to become more positive. Perhaps we should consider that some things are worse than recessions, and that there are several other gauges that should be put on the same level as a defined recession. As such, the SHB perception is that we are, and have been in for some time, something economically and negatively deep, that will be long and drawn out. Like sucking the poison out of a wound, the government has tried to avoid where possible, the immediate impact pain that we have seen in other great down turns. It is likely that this is down to the economy being so fragile, and the balance between people at home being able to struggle, vs breaking entirely and being unable to pay their financial commitments, being so tight. What is clear, is that this is likely to go on for quite some time, and this means further small incremental interest rate rises, more unemployment, ongoing Union strike action and the rest of it. This is all healing, and the property sector is likely to have a reasonable amount of success, as we fill our positions as advisors for our clients across the land. The bit that we should fear are the periods of uncertainty we have experienced in this first qtr. The fog will clear and beyond it, the promised land of organic growth. For now, we need to be mindful and very careful about how we all spend our money. Away from the super kit, the market is likely to start tightening its grip.