Market activity, sector take-up, rent trends & predictions

Q3 2025 saw London’s office occupiers sharpening their focus on quality, flexibility and cost efficiency. Prime locations remained in demand, but there was a noticeable uptick in activity from a broader mix of industries, reflecting a more diverse and competitive landscape committing to their next business moves.

For companies prioritising prestige, flexibility, or savings, knowing how rents are shifting across London is vital to making informed real estate decisions.

Below you’ll find a detailed overview of current market trends and key statistics including:

– Key London market stats »

– London office rents & rates guide »

– Notable Q3 London office deals »

– SHB client results (£8M saved!) & sectors we moved »

– Q3 market vs Q2 predictions »

– Outlook for the rest of 2025 »

Read on for the market stats to help support your next office move…

London office market snapshot

We ran the numbers, tracked market activity, and spoke with many businesses. Here is what we found…

Q3 2025 saw London’s office market maintain momentum, though at a slightly slower pace than the previous quarter. Activity continues to be shaped by occupier demand for quality, flexibility and value, with headline numbers reflecting both resilience in core submarkets and ongoing pressure on secondary space.

Key market activity from across London

Take-Up: 2.7m sq ft

Down from Q2’s 3.2m sq ft, but still robust and above the 2.4m 10-year average.

Vacancy Rate: ~9% (London-wide weighted)

Stable but elevated compared to long-term averages. Available sq ft is sitting at 23.9m, which is above historical norms.

Prime Rental Growth (City, YoY): +8.3%

Sustained upward pressure in top central locations

Rents & Rates Guide

Speaking of rental rate shifts, we’ve gathered up the headline rents across submarkets and available stock on the market. See how each prime London office market values their Grade A Fitted, Grade B, Managed Offices and Desk Rates in our guide here ↓

Q3 key London office deals

HSBC Bank

40 Bank Street, E14 Docklands – 209,200 sq ft- Letting

The quarter’s largest letting, anchoring Docklands activity and driving the submarket’s out-performance in Q3.

↓

InfinitSpace

Fox Court, 14 Gray’s Inn Road, WC1 – 101,778 sq ft – Letting

Big flex-operator expansion, signalling sustained demand for plug-and-play space at scale in the Midtown fringe.

↓

Bristows

Bow Bells House, 1–11 Bread Street, EC4 – City – 68,600 sq ft – Pre-Let

Legal sector commitment into high-quality City stock, consistent with the flight-to-quality theme.

↓

BMS Group

The Gherkin, 30 St Mary Axe, EC3 – City – 64,300 sq ft at £84.00 psf – Pre-Let

Blue-chip insurance move in a landmark tower with a clear prime rent signal.

↓

RWE Supply & Trading

The Northcliffe, 26–30 Tudor Street, EC4 – Midtown – 55,900 sq ft at £74.06 psf – Letting

Energy trading footprint in quality space; good evidence of diversified demand beyond core finance/tech.

↓

MSCI

Exchange House, 12 Primrose Street, EC2 – City – 51,800 sq ft at £87.50 psf – Letting

Data/financial services occupier paying a robust headline rent in a prime City asset—classic flight-to-quality.

↓

General Atlantic

The Elephant, 318 Oxford Street, W1 – West End – 52,173 sq ft at £165.00 psf – Pre-let

High West End rent marker on Oxford Street, underscoring the pricing power of top-tier West End locations.

Q3 SHB client results

Money saved & sq ft exchanged

£ saved for clients in Q1-Q3 2025

desks moved +150% up from Q2

£ saved for clients in Q3

sq ft transacted

Last quarter showed a shift to advisory and long-term planning

→ Diversity of demand

Our client base remained broad, with financial and property sectors continuing to drive the majority of activity. Technology and business services are showing renewed momentum, while education, hospitality and not-for-profit sectors were more active than in previous quarters.

→ Strategic lease advisory

There was a sharp increase in lease advisory work suggesting that occupiers are seeking greater support in renegotiating terms and restructuring leases amid ongoing market uncertainty.

→ Mixed market sentiment

An uptick in acquisition and lease advisory work points to greater confidence among occupiers in making long-term decisions, even as some sectors remain cost-sensitive and are evaluating a renewal or a move.

What we worked on in Q3

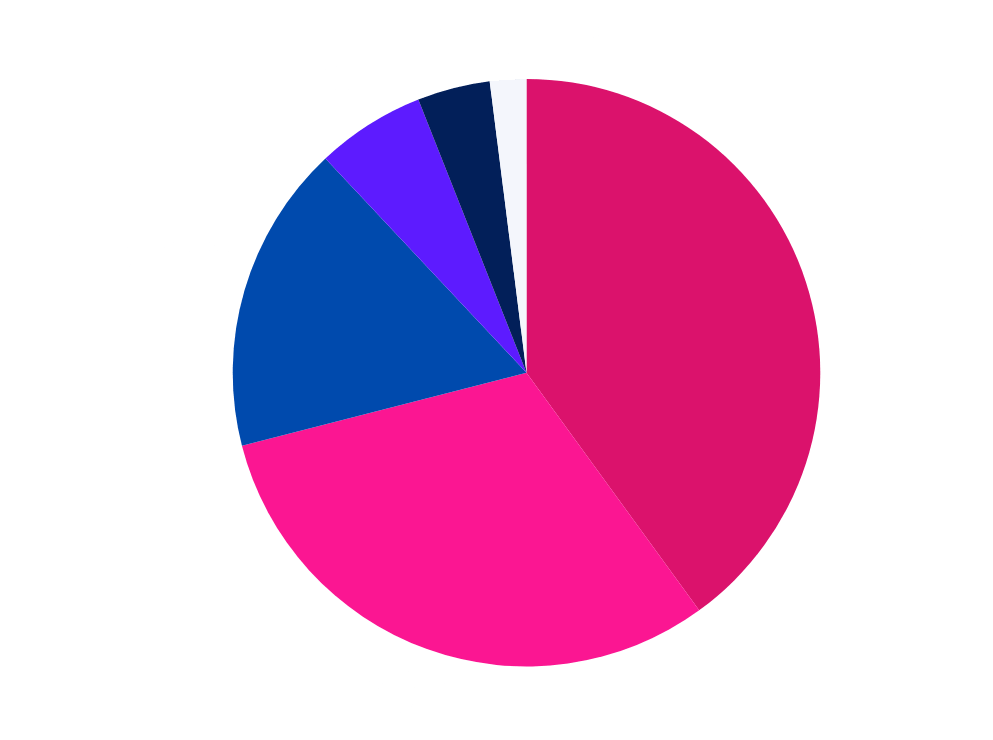

Sectors moving

Industries we found offices for in Q3 2025

↑ IT & Tech showed the most significant increase, doubling its share and reflecting renewed demand for flexible and tech-enabled workspaces.

↑ Business Services and Property & Real Estate both grew modestly, indicating steady activity and sector confidence.

↑ Banking & Finance remained the largest single sector but saw a slight decrease, suggesting some cooling after a strong Q2.

↑ Education deals were crossing the line, with a notable increase in completed moves.

Sectors we found offices for

Q3 market vs Q2 predictions

Q2 Prediction: Managed & Flexible Solutions Would Remain Attractive

👍 Q3 Reality: Managed and flexible workspace demand continues to hold, especially for mid-size and hybrid occupiers seeking agility. However, while plug-and-play solutions remain popular, Q3 saw a further return to traditional leasing in prime submarkets, with large corporates locking in long-term space to secure quality and ESG credentials. The managed model is still a significant part of the market, but the “flight to quality” in traditional leasing outpaced growth in flexible this quarter.

Q2 Prediction: Pent-Up Demand Would Convert into Transactions

🫸 Q3 Reality: Take-up in Q3 reached 2.7m sq ft – lower than Q2’s post-pandemic high, but still robust and above long-term averages. The conversion of delayed requirements continued, though at a slightly slower pace. Major transactions in the City and Docklands, including large pre-lets and relocations, confirm that pent-up demand is still being released, but the pipeline is normalising as more occupiers have now executed on deferred plans.

Q2 Prediction: ESG and Quality Would Remain Critical Drivers

👍 Q3 Reality: The trend strengthened further. Over 75% of take-up was for new or refurbished, ESG-compliant space. Rents for Grade A, best-in-class buildings set new records in the West End (£250/sq ft top end) and City (£130/sq ft top end). Non-compliant and secondary stock remains difficult to let, with landlords under pressure to upgrade or reposition. ESG is now a baseline expectation for most active occupiers.

Q2 Prediction: Prime Rents Would Continue to Rise

👍 Q3 Reality: Prime rents in the City and West End saw further upward movement. City Core Grade A fitted rents reached £130/sq ft (up from £120 in Q2), and West End Core saw values up to £250/sq ft (vs. £260 in Q2 and £200 in Q1). Midtown, Southbank, and fringe markets also saw a steady upward drift, though the pace of growth moderated slightly compared to the Q2 surge. The premium for best-in-class space is widening as occupiers become more discerning.

Q2 Prediction: Submarket Divergence Would Persist

👍 Q3 Reality: The divide between prime and secondary space remains stark. Vacancy in new/refurbished stock is low (City new/refurb vacancy: 4.9–5.5%), while overall vacancy hovers around 9%. Docklands saw a 135% YoY surge in take-up, driven by value-seeking corporates, but vacancy remains elevated in older buildings. Fringe and emerging submarkets offer value, but pricing power is squarely with landlords of high-spec, centrally located assets.

Q2 Prediction: Investment Market Would Remain Subdued

🫸 Q3 Reality: Investment volumes are still below long-term averages, with capital targeting value-add and ESG-compliant assets. Investor caution persists, but appetite for prime, sustainable buildings is strong.

Outlook for the remainder of 2025

It’s going fast! As we’re now in Q4, the London office market remains competitive, with occupiers prioritising flexibility, quality and saving every penny. Businesses should continue to adapt their workspace strategies for the year ahead and future-proof their operations by getting more value from their office. We think a few trends will carry over into the new year…

Take-up: Expected to remain above the 10-year trend of 2.4m (2.7m in Q3), with some seasonal and budget-related slowing in Q4.

ESG-led refurbishments: ESG compliant completions will total 2–3m sq ft by the end of H2. Workspace requirements and new furnishings will be considered to make the most of existing or new space.

Prime rents: Upward pressure likely to persist, especially in City & West End.

Secondary space: Grade Bs will get a final call for modernisation before it’s too far behind the other stock. 🚂

Occupier strategies: We expect businesses to focus on aligning workspace with strategic goals – balancing cost, flexibility, and quality. Increased operational costs will see an uptick in workplace strategies and require careful negotiations to find savings where possible.

If we can help with any office questions, workspace strategy hurdles or opportunities we see in the current market, we are here to help. Please get in touch with the team.

We’re here to help – give us a call!