Central London Overview

The first quarter was overall very good, and we saw the wider markets rally very nicely, and from the moment we all got back from the festive break there was a very pleasant and familiar fizz in the air. It felt great to be back and most markets had a pretty funky time, with voids being pinned back, rents holding and, in some cases, making a forward step, and we saw rent free periods begin to stabilise.

From a performance point of view, as we have become accustomed, the Cat A + products in general have led the way, particularly where there has been real attention to providing a high-end product. In these cases, the rent profiles have been maximised and the frontloaded expenditure repaid and more. Still however, many landlords are not understanding what is required from this permanent change and expectation in the market, which is necessary for them to implement in order to allow their assets to perform to the highest degree.

The more secondary stock in tertiary locations is having a trickier time and we started to see the quoting rents in those buildings being reviewed and incentives being pushed out in order to attract occupiers to make a willing move; a trend that once starts, is likely to gather momentum. For now, we can be very happy with the performance of the first quarter and with an enormous amount of pent-up demand driving it, nobody should be disappointed.

Market rents

Market rents, overall, have seen some important uplift. As we come to the end of the first quarter of 2022 it is safe to say that quite a lot has happened in the past 3 months. January saw the Omicron strain of C-19 dwindle almost as quickly as it started spreading. Then a few weeks of relative ‘normality’ followed by Russia’s invasion of Ukraine in late February which has continued into the present day.

With that being said there has been some significant uplift in certain submarkets. There is an apparent theme occurring from Q1 2021 to Q1 2022 and that is that Grade A top-spec office space is seeing considerable increases across multiple submarkets. Most notably, and for the third consecutive quarter, Mayfair. Across all the submarkets Mayfair’s Grade A stock has had the largest percentage increase in rents. One of the factors influencing this increase is the number of new schemes entering the submarket, which are commanding big rents. Every other submarket in the West End has increased in the previous quarter.

Away from the West End, the City Core has seen typical Grade A specification stock quoting rents increase too (for the first time in three quarters). Clerkenwell, Shoreditch, Spitalfields and Aldgate otherwise described as the City Fringe have not had such a strong quarter with small decreases in the typical rents for Grade A stock respectively. Midtown has remained relatively the same with the exception of Bloomsbury which has seen a substantial decrease in typical asking rents – largely driven by a lack of demand from occupiers.

When it comes to Grade B stock or secondary stock the picture is less rosy. Although no significant decrease from the previous quarter, there hasn’t been any increases either. The majority of submarkets have experienced a 5% decrease in typical asking rents from the previous quarter. This is arguably due to the increased availability of second-hand stock.

All in all, the data shows that is if there is a top-spec kit out there in the right location prospective tenants would pay over what is expected.

Leasing activity

The restrictions imposed in late 2020 and 2021 meant that many occupiers continued to push back their return to the office plans until later in the year. Thankfully as the year developed so did occupiers’ confidence due to the comprehensive rollout of the vaccine.

To put this into perspective activity within the central London market during Q1 2022 reached highs of 2.9 m sq. ft, representing a momentous YoY increase of 92% which demonstrates the clear resurgence in leasing activity.

Contrary to this, vacancy levels across the London market have remained high, however largely the same over the previous years, with availability at a record low within recent years, reaching 7% in Q3 2019. Ever since, availability has continued to cultivate, with the most recent quarter reaching circa 10.9%.

At the end of Q1 2022 central London availability reached highs of circa 27 million sq. ft. This remains considerably higher than the decade average of circa 15 million sq. ft. With supply of all types of quality (both newly refurbished, and second-hand tenant space) rising in excess of 7.55% during the latest quarter. The largest increase in new availability was in fact fuelled by a 50% increase in availability for pre let opportunities. Contrary to the typical COVID story, the second-hand disposal market dropped by 5%. Perhaps a sign of recovery and/or just indication that occupiers have decided to re-occupy their existing offices following the end of government restrictions

It’s clear there continues to be an occupier preference for quality led assets, with an ever-increasing emphasis on sustainably aware office accommodation, despite occupiers often choosing to reduce their overall footprint as they choose to operate a hybrid working model.

Despite the success of an agile working process and an ever-evolving market uncertainty, the leasing market as a whole very much rebounded during 2021. Take up reached a two-year high in Q3 2021 with a specific reference to September which saw the highest activity since the inception of the Pandemic. There was in excess of eight lettings over 100,000 sq. ft within the quarter, this is equal to the last five quarters combined, as many of the larger occupiers decided to capitalise on the uncertainty and take a longer-term view.

In comparison, in Q1 2022 the only deal over 100,000 sq. ft was Hogan Lovells pre-let 280,000 sq. ft at 21 Holborn Viaduct, EC1, the latest in a line of large acquisitions by all the law firms. Since early 2020, there have been circa 10 transactions over 60,000 sq. ft, specifically to law firms, amounting to 1.9 million sq. ft in total.

A further show of strength and renewed sense of confidence within the market can be seen in the level of office space currently under offer. According to a leasing data source, this has reached circa 4.1 million sq. ft. This is well above the 10-year average of 3.4 million sq. ft. This increase has been reflective over the last three quarters.

Vacancy rates and availability

London’s office vacancy rate continued to rise during 2021, despite a very strong rebound in leasing activity in Q1 2022. After bottoming out at around 5% in 2019, the vacancy rate has since jumped to 8.2%, its highest level in 10 years. The spread between vacancy rates in large and small buildings sank to its lowest level in more than 15 years in the second half of 2021 amid a sharper rise in vacancy in the latter.

However, net absorption has remained positive in the best-quality offices with firms demand pivoting towards better quality, sustainable space in a post-pandemic world, even if many shrink their overall office footprints as flexible working persists.

It is noteworthy that ‘ready to occupy’ quality office space vacancy levels are at a record low as firms pivot towards ‘turn key’ solutions which do not incur the same level as capex attributed with fitting out and furnishing a CAT A office.

Sales market and construction pipeline

Development Pipeline

Since Q4 2021 there has been very little difference in terms of the stock on the market that is under construction or refurbishment with just under 13m sq. ft under construction. The market is showing strength since Covid with a third of this number currently under offer before completion finishes.

35% of this construction should deliver to the market during 2022 meaning that supply should increase from its current figure, however with demand picking up as the year progresses we may find by the end of the year that the amount of space on the market remains relatively static.

The largest development to complete in Q1 2022 was the combined CBRE GI, King Street RE GP & Arax Properties scheme at 280 Bishopsgate. This building comprises 254,000 sqft of newly created space and at the time of writing SHB visited the building and can confirm that less than 10% of it is still available after significant lettings to Baker MacKenzie, digital group Cognizant, FTSE 100 asset manager Abrdn and Getty Images.

Sales Market

Q1 2022 has seen unprecedented investment activity culminating in a record first quarter figure of just over £5.5bn committed in central London sales. What a difference a year makes as this most recent quarter has recorded well over the £3.9bn committed throughout the whole of the last half of 2021 showing a significant uptick in investor confidence.

These figures were mainly buoyed by a larger than normal completion of larger deals with 13 deals over £100m compared to just two deals over £100m in the previous quarter. Overseas investors swarmed the London market making up over three quarters of the deals completed showing that the UK and London specifically, with Covid waning and despite the threat of hybrid working, was the place to invest their capital.

The largest deal in terms of amount paid was the sale of 5 Broadgate for £1.21bn to NPS, the Korean pension fund who acquired the 733,000 sq. ft UBS Wealth Management occupied building from CK Asset Holdings. Not a bad return for the Hong Kong investor with a 20% return in just shy of four years! Another notable purchase/sale that went through this last quarter was Google buying their own current London HQ in Central St Giles for a reported £730m despite having their own super HQ under development in Kings Cross.

Flexible office market

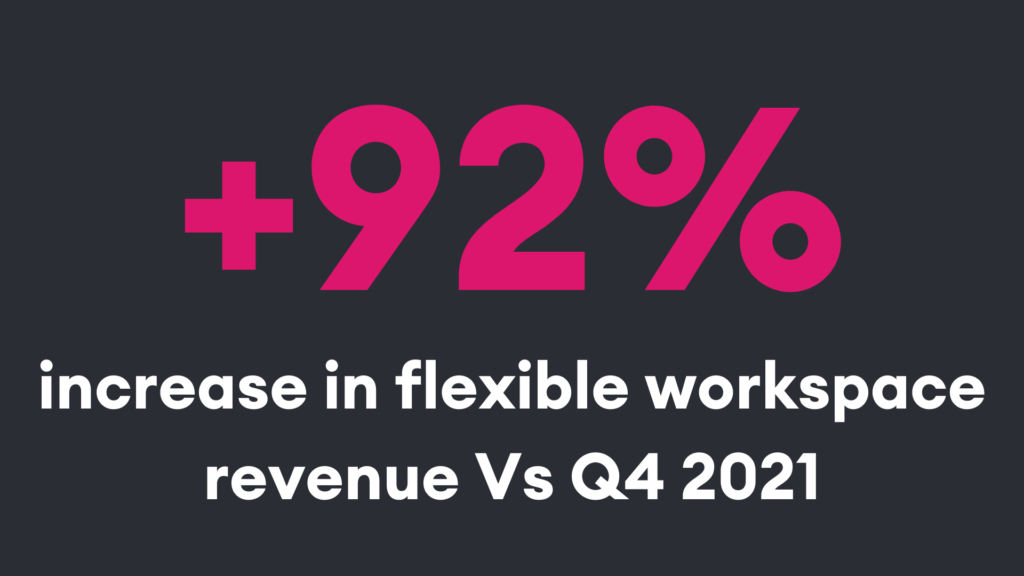

The quarter started slowly for the flexible market with January and February being very quiet, however March picked up considerably with a record number of viewings and completed deals for the department. In the month of March alone 12 serviced deals were transacted in comparison to 16 deals for the entire Q4 2021 period. Q1 2022 saw a total of 20 deals – a 25% increase on Q4.

There was a slight dip in the number of desks acquired with 356 for Q4 and 323 for Q1 – just over a 9% decrease but remaining fairly steady in general. However, more notably there was a 92% increase in revenue on the previous quarter.

The huge increase in deal value was partly down to some larger requirements but also likely due, in part to clients looking at quality over quantity. Many clients moving away from a conventional model are looking to downsize considerably which is a cost saving, leaving room for them to focus on smaller high-quality serviced office space with good facilities.

The submarket spread is more even than the previous quarter with no specific submarket being more popular than another, however West End as a whole is still proving more popular than City and Fringe locations, although enquiries for these areas are also increasing. This is likely due to the slower return of the industries that typically dominated City markets and also because the price point is more affordable and there is more availability in comparison to areas such as Soho and Victoria.

Industry analysis

As per our above comments on take-up and leasing activity, this was the quarter of the SME, with majority of deals completing sub 20,000 sq ft and a good mix of sectors taking up space showing strong commitment cross-sector and the return to the office for a lot of firms who exited leases since the start of the pandemic.

The legal sector dominated once again helped by the only deal which completed over 100,000 sq. ft which was the aforementioned pre-let of 280,000 sq. ft at 21 Holborn Viaduct by Hogan Lovells

Most areas of business were up in London over Q1, with things falling off towards the end, as a result of the invasion of Ukraine and the financial implications of the global pandemic starting to sink in following the Chancellors Spring Statement. We saw a small increase in domestic demand and 23% of London firms reporting an increase in domestic sales and recruitment continuing to climb closer and closer to pre-pandemic levels.

Now you would have thought that following the war in Europe, fuel & energy increases (69% of firms reporting increased energy costs in Q1), an expected inflation peak of 8.5% and GDP expected to grow by less than 2% that we would all expect the aforementioned growth stats & leasing activity to start dipping in the coming quarter, but I wouldn’t be so sure!

Business confidence was higher in Q1 that it has been for years with over 40% of London Businesses expecting turnover & profitability to improve in the coming 12 months and 33% of firms expecting London’s economy to improve.

Sectors that continue to grow and who us as a firm have experienced increased demand from include the Energy Sectors, Banking, legal & healthcare.

As we move in to Q2, one thing I think that we will all hope for is more clarity – from the conflict through to any assistance the government will be looking to provide to businesses moving in to what looks to be darker days.

Simon says

How often in the professional, political, or economic worlds do we hear the words, ‘that won’t happen’, or ‘that isn’t possible’? This kind of narrative is often said with an almost belligerent disregard, and in recent times, has proven to be inaccurate again and again. Take your pick from the election of Trump, BREXIT, a pandemic, and now the Russian invasion of Ukraine, we now need to get some far clearer and more realistic views and discussions moving forward. One of those discussions should be when will the recession properly start and what kind of recession it will be. An entirely subjective discussion but this is purely based on the economic pieces being very well placed for such an occurrence, with inflation being crazy high, interest rates very much on the move, the post pandemic fall out beginning to settle in, BREXIT impact and now the unwanted conflicts within Europe that are currently escalating faster than perhaps we would like to admit.

Meanwhile however, there always appears to be a delay on market interaction with such things, and currently the property market is still concluding the deals that were agreed in the first quarter. Be aware that this could be misleading and within SHB, we have seen a clear shift in the attitude and approach of occupiers with events towards the second half of the year, where the commercial objectives are more around the idea of remaining in situ rather than relocations, of the kind we enjoyed in the first quarter. Occupier sentiment seems to have very quickly shifted back to a more defensive approach, and rather than exploring with excited vigour of a relocation due to growth, at SHB we are being directed to shorter lease extensions and a further positive move towards serviced offices, which continue to benefit from these tricky times.

All of this is likely to continue for the foreseeable, and the harsh reality is that we will very soon need to go through significant pain, to reach the promised land of pure and natural growth again. For now, let’s just acknowledge that with the pandemic feeling like a dystopian nightmare memory, we now have more pressing matters to pay attention to within the European block, so let’s watch, help where we can and hope that things calm down. It really would be nice to have a few months where not a lot happens around the world.