Central London Overview

Where the year began in good spirits, with deals still moving across the line with relatively minimal risk of falling out of bed, what we have seen develop in qtr. 2 has presented something quite different. Although it has felt that there are still a fair abundance of deals happening throughout London, outside of the core West End markets, the right deal levels feel more uncertain. On one hand, we have bullish landlords pushing for value, and on the other, slightly more realistic building owners that can feel that things are changing and chasing a market down is never the best route to success. To be fair, with the supply of high-end products still exceptionally low in certain core markets, such as the West End, it is increasingly confusing as to where values and incentives lie. For example, if we look at some of the periphery markets such as Hammersmith and even Shoreditch (always indicators for difficulties that might be coming), we are seeing fast approaching availability and voids beginning to look a little more uncomfortable.

Meanwhile, as the conventional world begins to creak and strain under the rising tide of economic uncertainty, the post pandemic popularity of Cat A+ and serviced/managed solutions continue to rise. Looking ahead it feels unlikely that this is a trend that will change, but there is no doubt that the quickly rising price of the serviced product is not likely to have a great chance of longevity survival when rents start to drop, and available conventional lease terms come in. For now, the demand remained strong, and although available cash for most small to medium size firms is looking tighter than for some time, this has all in all been a productive and profitable quarter for most.

Market Rents

At the end of Q2, market rents overall haven’t differed too much from Q1, where rents across the board saw significant rises from the previous quarter. The strength and resilience of the market continues to show.

In the West End, prime West End submarkets continue to command the highest rents. With Mayfair, St James and Fitzrovia demanding the highest rents which the market is getting very used to. Typical rents in Mayfair are regularly getting to over £150 PSF for upper floors.

Furthermore, the three months to June 2022 marked the strongest Q2 take-up volumes since 2017 and activity was 55% ahead of the volumes recorded in the corresponding period in 2021. The total of 1.2 million sq. ft was 50% above the previous quarter’s total and 36% above the 10-year quarterly average. This brought year-to-date volumes to 2.0 million sq. ft, 55% above volumes in the same period last year and above the 10-year H1 average of 1.8 million sq. ft.

In the city, rents have stabilised for a second quarter. The figures show that the predicted spiralling downfall of the city which some believed in, was erroneous on all accounts and typical rents are mostly at pre-pandemic levels. Top-spec space in city prime continues to achieve £75 PSF.A total of 1.4 million sq. ft of space was transacted across the City in Q2 which was a 12% drop on the 1.6 million transacted in the previous quarter. However, this figure remained 91% ahead of the 715,000 sq. ft leased during the same period last year and in line with the 10-year Q2 average. As a result, year to date volumes reached just under 3.0 million sq. ft, which was almost double the same period in 2021 and 13% ahead of the 10-year H1 average of 2.6 million sq. ft.

Leasing Activity

Thankfully the London leasing market has continued to recover from its torrid recent history within the depths of COVID. This can be realised within the previous 3-9 months. Despite seeing occupiers shrinking their office footprint by 30% on average, there has been a continued and ever-growing sense of optimism surrounding the marketplace.

Whilst this may not be reflective of all occupier types, its clear certain businesses have fared better than others. Technology, media and legal firms all experienced significant activity, helping push leasing figures especially at the larger end of the market. With occupiers such as Facebook and Snapchat making large acquisitions within the last 12 months. Not to mention, large pre-lets to the likes of Hogan Lovells, Kirkland & Ellis and Blackstone.

Contrary to the encouraging levels of activity, vacancy rates across London have increased over the previous 12 months equating to 8.1% which can be compared to Q2 2021 of 7.5%. This is partly due to delayed completion of several new developments being delivered to the market. Following a hiatus of development during the peak COVID months. A similar picture can be seen with the availability rate, which currently lies at 11% in Q2 2022, compared to 10.6% back in Q2 2021.

Average market rents across London have remained relatively consistent YOY, however we have seen early signs of reductions. Further loses are expected in the coming months / years as the country deals with the fall out of an ever-uncertain economic climate. This has been seen by the relatively adverse change in average market rents of London, failing from £50.39 PSF, compared to £50.62 PSF in Q2 2021.

We must caveat; however, we expect to see a continued confusion/concern from occupiers as they continue to understand their use of the office post COVID. This is due to another factor, with occupiers reducing their footprint to react to agile working (on average of 30% since the inception of COVID). As a by-product many are adopting a more capital-intensive way of occupying their offices, investing in their fitout with the hope of encouraging employees back to the office.

Of course, there continues to be a lack of supply for best-in-class office, hence the achieved rents and overall transaction information demonstrates that. This is largely driven by lack of supply but also by the ever-looming changes in sustainability requirements. Whether tenants have a strong CSR outlook or alternatively they are pushed, completely out of their control by the newest changes by government. The onus of which has yet to be proved, with canny landlord’s requiring tenants to undertake the works themselves. A cost of which has yet to be confirmed. Either way, in the later part of the 2020’s, buildings will require a minimum of a B EPC. Interestingly enough – the government expects more than 80-90% of buildings within London will need to be comprehensively overhauled in order to hit the required EPC criteria.

To conclude, whilst the market has grown leaps and bounds since the emergence of COVID, it’s hard to imagine the Central London Office Market won’t be adversely affected by the current economic climate aka rising inflation, record borrowing and questionable government.

Vacancy rates & Availability

Despite still exceeding the 10-year average by + 3%, the London Office Vacancy Rate is beginning to stabilise following robust leasing during Q2 (standing at approximately 8.1%). Total supply across all specifications of space is standing at 19.8 million with ‘second hand’ tenant space declining for another quarter. New build supply continues to be robust (1.5%) as a result of occupiers focusing on ESG credentials and quality of space in assisting the return to the office. The reduction in overall vacancy rate compared to Q1 2022 and throughout 2021 suggests that organisations are returning to central business districts, but we should be cautious and note that Q2 2022 results are underpinned by significant lettings such as 221,700 sq. ft in the West End (Paddington Square) to Capital International at Paddington Square and 413,300 sq. ft to Kirkland & Ellis in the city.

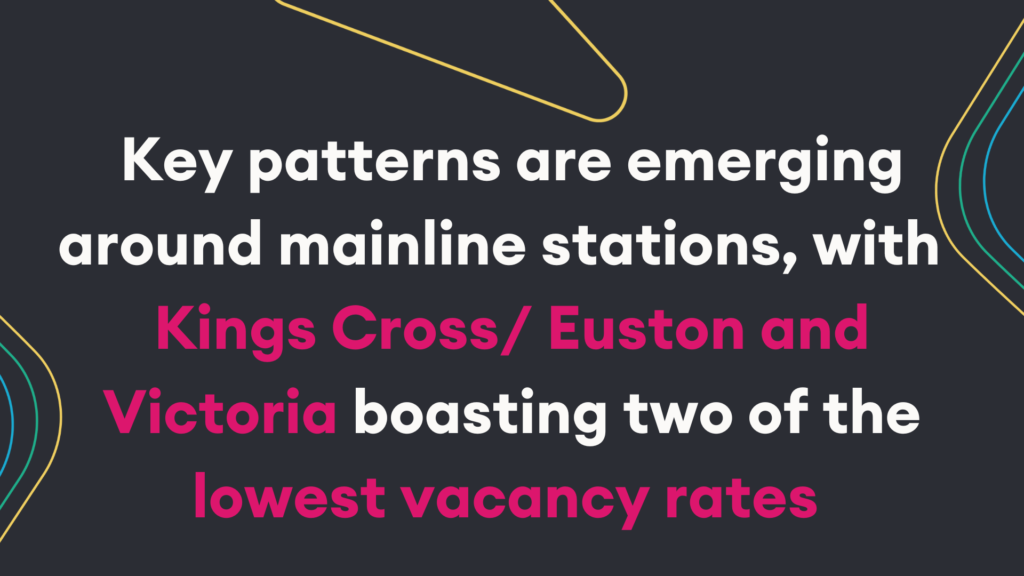

Data shows that key patterns are emerging around mainline stations and accessible areas with submarkets such as Kings Cross/ Euston and Victoria boasting two of the lowest vacancy rates at 3.8% and 4.4% respectively. Take-up in City Core and Canary Wharf is improving however they still have two of the highest vacancy rates in London at 9.6% and 13.3% (albeit some Landlords see this improving as a result of the successful opening of Crossrail). Submarkets such as the core West End continue to perform well due to the lack of supply and demand levels being high. The sub-20,000 sq. ft market continues to improve, and vacancy rates are continuing to decrease across London for CAT A+ and plug and play space. This is a result of increasing costs associated to construction work and acquiring space.

Sales Market

In general, we have seen investment activity compared with previous quarter soften quite considerably with £2.6bn worth of deals go over the line in Q2 which was down just over 50% compared with Q1 2022 (£5.5bn). There were eight deals exceeding £100m with more than 50% of this transacting in the West End alone (just over £1.5bn) and out of that £2.6bn total, 72% of it involved overseas capital. Asian and North America accounted for 66% showing where the money is coming from and also showing that European money since Brexit is well below previous years.

With word on the street being that finance is becoming harder to come by, with the banks conscious of increasing interest rates coupled with investors trying and work out the future of the landscape over the next 12 months and whether now is a good time to allocate capital to commercial property investment purchases, it is not surprising that we saw Q2 soften in terms of deals done. This has also been seen in the industrial and logistics industry too. The question will be whether investors see this as being the time for allocating capital elsewhere within their portfolios to diversify risk or whether some want to call the top of the market and cash in before it’s too late. They will all be keeping one eye on the completions of new buildings, the slowing of pre-lets and the potential for supply to increase so that they can make these calls as to whether they will get the ROI they need on deals.

Some of the noticeable deals to go ahead this last quarter were Goldman Sachs/Greycoat purchasing Sancroft in Newgate Street for £370m, GIC Real Estate purchasing a share in 2 Kingdom Street in Paddington for £275m, Kingboard acquiring 2 London Wall Place for £302m, Derwent buying Moorfields Eye Hospital for £239m for future redevelopment and 70 Gracechurch Street changing hands for a tidy £300m to Stanhope.

Construction Pipeline

Despite the cost-of-living crisis that is upon us all, the number of buildings under construction rose slightly to 13.5m sq. ft since our last report (13m sq. ft) with the Midtown submarket seeing no less than 7 new schemes under way. Noticeably only 5 schemes that have gone ahead in the last 6 months have been new builds, with the majority being refurbishment of existing buildings. One likely reason for this is purely down to the cost of steel and concrete being exorbitantly high compared with previous years as well as Landlords trying to work out what net zero actually means and keeping up with the ever-increasing demands of occupiers looking to meet ESG quotas.

Given the obvious woes in the economy and what may be coming round the corner, one statistic that might cause landlords some concern is the amount of newly completed offices hitting the market is expected to reach nearly 7m sq. ft which will be the highest since 2003. This may be subject to delays in construction though, due to labour shortages and supplies of materials (borne by the combination of Covid and the War in Ukraine). Two of the largest to complete this year will be 8 Bishopsgate (770,000 sq. ft) and 21 Moorfields (564,000 sq. ft). Whilst this will help some submarkets with relatively tight supplies, it may come at a time where further space comes onto the market from occupiers feeling the pinch and 2023 might be the year where we see supply and demand shift in opposite directions thereby allowing occupiers who need to move more choice and better deals and force some landlords to be a little more pragmatic about driving their rental income higher.

The figures from Q2 2022 in terms of lettings remain strong but the big question is how long will this continue?

Industry Analysis

As per the office take-up statistics, things stayed strong cross-sector over Q2. We saw our robust legal sector remain at the top of the charts with large deals from the likes of Holman Fenwick and Kirkland & Ellis. Closely followed up the financial sector. There were also some great flex & conventional leasing deals completed within TMT sector at both the higher level and smaller churn level.

There’s a huge amount going on which will impact decision making in Q3 with the on-going leadership debate and lots of pressure on businesses, with 82% of firms citing inflation as a growing concern and 62% expecting to raise their prices. With no certainty on the short to medium term outcomes of such decisions, it’s difficult for many firms to commit to long term decisions especially when staring down the barrel of a 10-year lease. As such, it’s our expectation to see a lot more activity cross-sector at the smaller end of the scale and a lot of the larger firms perhaps opting for an extension of their leases as opposed to a renewal or move. The flexible office market will of course benefit from such uncertainty.

In the world of private equity, we are still seeing lots of investment with deal numbers increasing in certain sectors and staying steady in others. The average amount invested has dropped off slightly, but this follows a couple of record-breaking quarters, so we were always due some kind of correction. What we are seeing are lot’s more deals at the smaller end of the scale i.e., £250,000-£2m which is truly encouraging and could possibly be linked to a number of start-up’s born from the pandemic.

Top 3 sectors for investments (including some huge deals) are Fintech, AI & Clean Tech. Digital security, which was once the emerging sector expected to really compete at the top, has fallen away with a decline to pre-pandemic levels, the same for Blockchain. Looking ahead I don’t think our top 3 will change over the coming quarters but imagine that we will see a bit of a slowdown in activity in Q3 as investors start to tread more carefully until there is some certainty on where the economy is heading, and the implications of what decisions are made by whoever is appointed to lead the country after Bojo’s exit.

Flexible Workspace

April was a slow month in comparison to the previous month, with an unusual number of public holidays we felt the effects of people taking advantage of the “free” annual leave. May and June however saw a resurgence in activity, and we closed the quarter with a total of 19 flexible office transactions, just one shy of the previous quarter – a quarter with a record-breaking month.

While the number of desks acquired was lower than the previous quarter the average desk rate increased by over 7% supporting the narrative that the market is rebounding since the pandemic and the demand vs supply is encouraging a rise in overall desk rate.

We are still seeing a reasonably equal number of enquires and transactions across the various submarkets, however it is clear that Mid-Town is growing in popularity, partly because of the more cost-effective price point but also due to the availability – many clients looking in the West End, specifically Soho are looking towards Mid-Town for affordability and availability.

Simon says

SHB and the general market have enjoyed a strong quarter 2, however there are clear indicators that there is deep recessional danger not far away. The chances are we are already in a recession now, and it is not the immediate recession we should fear, but both what kind of recession this one will be, but also when will the immediate impact be felt. What we are feeling now in terms of inflation and the cost of living are simply tremors for what is likely to be coming,

For now, it feels easier just to write a brief list to run through them, so let’s have a look.

War in Europe: Since the horrors of World War II, there has not been a war so close to UK shores. The physical distance of the war from the UK can be misleading, the media coverage probably not entirely accurate (who knows?) and the sanctions certainly not enough; it is clear this is an extremely dangerous situation. We have now normalised the fact the war is happening, but escalation is never far away. If you do not find this frightening and intimidating, then you really should.

Rising Interest Rates: It might be slow for now, but a clear indicator that we have lost control of our economy. The modern-day norm of exceptionally low interest rates is not a historical norm, and the increases are now likely to gather pace.

Inflation: Scary stuff on this one, with the figure changing depending on who you speak to but let us assume 9.2% for now and a likely increase to close to 11% by October. These rates are close to the things of legends and future comments like, ‘where were you when…’ may well be seen in the future. Regardless, it means that salaries cannot keep up with the inflation rises and with the ‘Cost of Living’ crisis already a painful subject, this really is just the beginning for inflation orientated pain.

Historical UK Debt: On one hand throughout the pandemic period, we very successfully supported jobs and individual income. On the other, we have fed the beast of over leveraging and UK debt. This horrific national debt issue has only been compounded as it simply builds on historical debt that reaches a long way back, including the banking crisis mountain because of quantitative easing. As if this is not enough, we have also the individual debt profiling that is just too high.

Company Debt: We are still reeling from the pandemic. There are deferred rents, deferred VAT payments, owed PAYE, falling behind with general bills and more. Unfortunately, the period of repayment sympathy seems to be over, and much of the above is being called in with increasing vigour.

Unemployment: Low unemployment is not always a good thing, and currently we have a country that is extremely good at employing people, but not particularly good at making money and contributing to GDP. With the combination of much in this list, the number of companies that will fail will begin to rise steadily, and therefore the number of unemployed will also begin to increase. Already many businesses are looking very closely at their costs, and that could see redundancies in the New Year.

Housing Crash: Much of what we have done in recent times has been to avoid the dreaded housing crisis, or the great correction. Much against the general view that in the late 80’s, interest rates will never get to 16-17% again, this is indeed true, however a far lower interest rate increase would trigger such a modern-day crash. The triggers will be complex and many, but they are largely rooted to unemployment and the ability of mortgage holders to maintain and keep up with their payments. With rising unemployment, this will simply not be possible, and the lenders are already not as friendly as they once were.

What does this mean for commercial office London?

The key word is ‘adapt’. The greedy landlords that look to maximise their deals, in some cases in exchange for weaker covenants, should be avoided. The occupier covenant strength, taking a lease should be paramount, and if this is at the mercy of giving away more incentives and accepting a lower rent, then so be it. From now until the run in to Xmas, we expect the number of transactions, along with the associated dealing terms to soften. The rise and popularity of serviced and cat A+ will continue as uncertainty again becomes a trigger word, which directly leads to many occupiers only wanting to offer short term certainty.

Summary

The suggestion of a hard-hitting recession can be intimidating, but there is no doubt that opportunities lie within. Not disregarding the job losses and the surrounding pain that comes with recessions, they are the most natural of things. Recessions offer true economic death and re-birth, and they then leave the foundations to build the next generation of market leading concepts, businesses, and individual performers. They are as exciting as they are brutal, and SHB is very much embracing the challenges.

For now, let us enjoy the active market that remains, but get ready, there is a storm coming…