In 2024, occupiers were assessing how hybrid working was changing their space needs. By 2025, many had tested new policies in practice. Now, moving into 2026, a clear pattern has formed: across flexible, managed and leasehold space alike, more businesses are choosing to stay and renegotiate rather than relocate.

The numbers back this up. Regears, renewals, restructures and renegotiations sit at the centre of London’s office market this year, whatever type of space you occupy.

Three forces are driving this: limited supply, higher relocation costs and the growing complexity of moving, regardless of business size. If you signed your current agreement during the return-to-office wave, you will already know that terms and incentives have shifted as demand has outpaced supply. Whether you are three months from a flexible licence break or eighteen months from a leasehold event, a strategic cost analysis now will help you unlock leverage and find the best path for growth.

Why more occupiers are choosing to stay

1 | The financial case for staying is shifting

Particularly for larger occupiers. A recent market update found that 25% of occupiers needing under 40,000 sq ft are likely to stay, rising to 46% for those needing more than 100,000 sq ft. Relocating a larger footprint is now more complex, costly and risky, particularly when it comes to finding suitable space in time. Smaller occupiers feel this pressure too. Many flexible workspace users are finding that renegotiating their current agreement, backed by current market data, beats moving when the costs land close together.

2 | 65% of occupiers with leases expiring by 2030 will face limited availability According to the same report. This puts regears firmly on the agenda. Grade A space is scarcer, decisions are being made earlier and pre-letting is increasing. Flexible and managed space feels this too: strong demand for the best buildings means providers are increasingly willing to negotiate retention terms with occupiers who can show they have genuine alternatives.

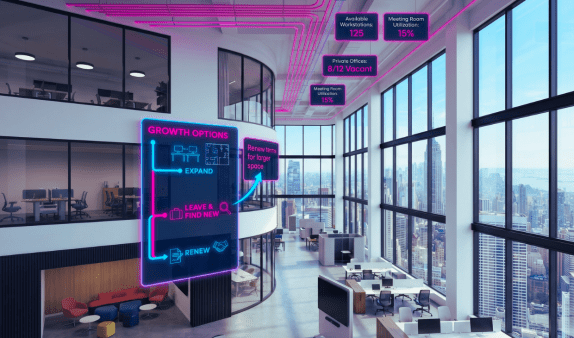

3 | The market has moved to a ‘pre-let first’ approach’ approach

43% of new London office space is already pre-let, and the 2026 development pipeline takes that further still: 70% of next year’s deliveries are committed before completion. Occupiers across the spectrum are securing space earlier. Leasehold tenants are pre-letting years out, managed space providers are filling their best floors early, and the strongest flexible buildings are running waiting lists for prime stock.

4 | Lease expiries are stacking up into 2030

More than 50 million sq ft of London leases are due to expire between 2026 and 2030, compressing timelines and pushing businesses to plan earlier, whatever they decide. How early depends on the type of space you occupy, which is where timing becomes critical.

Staying put is not the same as doing nothing. A regear, however your space is structured, is a chance to use the lease or licence event to improve how your space works for you.

We are seeing this first-hand, with a sharp year-on-year rise in reconfiguration projects across every space type.

Renew & Refresh – By the numbers

+114%

Fit-out project increase 2025 v 2024

Landlords and occupiers are actively updating space as they renew and reconfigure (SHB data)

70%

2026 development pipeline already pre-let

Using a different approach and trusted advisors is key

+79%

rise in Lease Advisory instructions handled by SHB, 2025 v 2024

50M+

sq ft of London leases expiring 2026 to 2030

Quick playbook for occupiers choosing to stay put

Here are the most common ‘stay and improve’ strategies we’re seeing in early 2026.

1 | Cost-saving exercises | Find money without finding a new postcode

Identify savings on rent, rates or service charges. The goal is to reduce leakage, tighten assumptions, and create budget certainty while the market is moving.

2 | Rent reviews | Reset to today’s reality

Renegotiate terms to reflect current market values and the building’s competitive position. In a polarised market, evidence and positioning matter more than volume. This is particularly important depending on when your last review was completed, to ensure you’re prepared to leverage other opportunities where levels have increased.

3 | Lease renewals | Stability with leverage

Secure more favourable terms for long-term stability, using:

• break options

• incentives

• capex commitments

• flexibility mechanisms

4 | Lease renewals aligned to new working patterns | Same lease event, different lens

Renegotiations that match how people actually use space now, not how they used it in 2021.

Start thinking along the lines of:

• rights to reconfigure

• utilisation strategy

• shared amenities or floors

• landlord-delivered upgrades

5 | Furniture and space reconfiguration

This is the practical layer that makes a regear feel like an upgrade:

• collaboration zones that actually get used

• quiet focus areas that aren’t afterthoughts

• phone booth strategy that matches meeting behaviour

• storage rationalisation and decluttering the floorplate

6 | Workplace strategy | Stay vs go analysis

Fully vet your scenarios of staying or going as cost modelling exercise alongside your operational impact.

• cost to stay vs cost to move

• availability of comparable office space

• people/talent impacts

• brand and client experience

• ESG / building performance trajectory

7 | Portfolio strategy + market intel

For multi-site occupiers, regears become a portfolio tool:

• sequence lease events

• consolidate where it helps

• keep real estate aligned to future plans

• anticipate supply pinch points before they hit

Three space types, three timelines

Whether you stay or go, the planning timeline and leverage differ by space type.

Flexible / serviced | 7 months out

Short notice periods mean the window for genuine optionality closes fast. Most of the decision happens in the final 3 months, but data-gathering should start as early as possible Check to see your licence notice window, which is typically 3 months.

Managed | 7 to 9 months out

Provider-led fit-out and onboarding add lead time beyond a straightforward licence renewal, even though the space is not leased in the traditional sense.

Leasehold | 9 to 18 months out

Full fit-out, dilapidations and a conventional lease negotiation cycle need the longest runway, particularly for larger footprints.

What to do now

Here is a starting sequence built to work across all three lease lengths and space types.

→ Market intelligence and supply scan – See what others are paying in each submarket, what’s available for your size band and space type.

→ Stay vs go model – assess overall cost, risk, operational impact and future alignment.

→ Learn market incentives available today – Rent free windows, incentives, capex and flexibility.

→ Space utilisation strategy – Document how the space should work for your people.

→ Lease or licence strategy – within your terms, look at options for renewal, re-gear, re-stack, or break and notice timing.

→ Fit-out options – Assess plans for updated furniture or reconfiguration.

Get an expert opinion

If you are weighing up your options – let’s run the numbers. Our team can discuss what the process looks like and where your opportunities are.

Fill in the form below or give us a call on +44 2035 148 867.